Finance and Controlling

Conessent’s knowledge and experience as specialists in design, conception and implementation of solutions, will deliver excellence for the harmonization of accounting within your business.

Overview

Compliance requirements in all countries are becoming more rigid, and finance departments are expected to become more effective in delivering on core information across the business.

In order to fulfill their role as an internal service provider, finance departments need to be accountable to various stakeholders, who need information for efficient and effective corporate management.

This becomes particularly apparent in the course of harmonization and internationalization of accounting standards. There are requirements for design and scope of controlling and accounting to be more dynamic, which influences the underlying ERP and reporting systems.

In addition to legal requirements and the far-reaching demands of external stakeholders for transparent corporate information, there are company and group internal harmonization efforts that result in the need for continuous integration, customization and extension of the existing financial and controlling applications.

- FSCM

- Harmonization

- Parallel Accounting & Segmented Reporting

- SAP Revenue Accounting & Reporting

- Lease Accounting & IFRS-16

Financial Supply Chain Management (FSCM) is geared towards optimizing the financial supply chain and cash flows within a company or group of companies thus optimizing the working capital in terms of cash and financing costs.

The efficient handling of billing and payment processes has a strong impact on KPIs such as the reduction of DSO (Days of Sales Outstanding) or an extension of the DPA (Days Payables Outstanding) and thus help to strengthen the internal financing capacity which – together with a more accurate liquidity planning – leads to a reduction in the cost of funds.

This FSCM is an integral part in the control of end-to-end processes across the value chain within a company or across enterprise boundaries. Representing here are (from order to payment) and Procure-to-Pay called (from the requisition for a payment) that processes the order-to-Cash – the optimization of these processes is driven by clear definitions and targets over a range of features and applications which include:

- Collection and Dispute Management

- Cash and Liquidity Management

- Treasury

- Risk and Credit Management

Benefit from…

…and access our extensive expertise in the field of optimization of end-to-end processes with special emphasis on cash flows and the strengthening of the working capital in your business.

Harmonization of accounting within your group will provide transparency, a streamlined reporting structure, and optimized business performance.

The conditions for the smooth and timely consolidation at group level must be firstly adopted at the level of the group units. This is not only about a consolidation of legal entities, but very often about accurate and reconciled reporting on profit center level and functional area on group level.

Comprehensive measures are taken to secure this, which include:

- The introduction of a single operating chart of accounts commonly used at the level of individual companies within a group

- The parallel use of a group chart of accounts

- Recording of all relevant information for consolidation already in the source system (partner object information captured on line item level of individual accounting documents)

- The automated billing of intercompany transactions

- The provision of user-friendly IC reconciliation reports and tools

- The group wide standardisation of business reporting

- A number of controls in the operating financial systems of the subsidiaries with respect to a smooth consolidation

- The provision of an integrated and automated interface in the group consolidation.

Benefit from…

…our experience as specialists in design, conception and implementation of solutions for the harmonization of accounting within your group.

International Financial Reporting Standards (IFRS) force the integration of external accounting with internal management reporting, directly influencing financial processes, design and content of both financial reporting and the underlying financial and controlling systems.

Segment Reporting

IFRS can be considered an example of this increasing convergence, according to which the definition of segments as well as the presentation of business unit information must be made on the basis of management reporting, whereas previously a (top-down) distribution of balance sheet positions on individual segments was considered sufficient. As a consequence – in the course of providing balance sheet information – companies must make enhanced use of information generated in controlling application and integrate it in external financial reporting.

Parallel Accounting

Today publicly trading companies are obliged to align their accounting according to international regulations (IFRS). In addition, local topics such as the Accounting Law Modernization Act (BilMoG) in Germany pave the way for convergence of local accounting law towards international methods of accounting. Although the HGB balance sheet still remains the basis for the calculation of dividends and the determination of taxable income, the commercial and tax balance sheets differ more from each other. This leads to the regular creation of deferred tax positions and ‘complicates’ the corresponding reconciliation between the two accounting systems. Given this background it becomes more important to consider a dedicated ledger for the tax balance sheet but in the same system, from which is reported in accordance with IFRS and HGB.

Cost of Sales

The international dominance of the cost of sales – and thus the structure of the profit and loss account by function areas of a company – requires close integration of internal and external accounting in order to ensure the derivation of functional areas for the presentation in the income statement from the cost accounting objects.

Talk to us…

…about your challenges with the architecture and design possibilities of your accounting system, with the aim of IFRS compliance. We are happy to advise and guide you through design and implementation.

SAP has launched Revenue Accounting & Reporting, an Add-on that has been developed primarily to reflect the requirements driven by a new revenue recognition standard and which acts as a dedicated subledger for revenue accounting.

The standard IFRS 15 – Revenue from Contracts with Customers – is introduced by the IASB (International Accounting Standards Board) in 2014 and provides accounting requirements for all revenue arising from contracts with customers.

It is meant to replace virtually all existing revenue recognition requirements in IFRS and US GAAP with a single framework which is based on five steps:

1. Identify the contract

2. Separate performance obligations

3. Determine transaction price

4. Allocate transaction price

5. Recognise revenue

IFRS 15 is effective for annual periods beginning on or after 1 January 2018 and is likely to affect the measurement, recognition and disclosure of revenue of all entities that enter into contracts to provide goods or services to their customers. This implies huge change and companies might face difficult challenges in order to prepare and apply the new rules.

The timing of revenue and profit recognition will hit companies across different industries. For entities dealing with various multiple offerings (i.e. sign up for annual plan and get devices for free), the main challenge will be to split bundled offers into individual performance obligations and allocate the transaction price accordingly.

A thorough analysis of existing contracts is necessary to conclude whether one or multiple performance obligations exist. Depending on when, and under which (organisational) circumstances a contract was made, it might be impossible or very difficult to identify the required information and the result might be fuzzy.

Judgement is needed when it comes to what revenue recognition pattern is appropriate for entities which apply to recognition methods, such as the percentage-of-completion method. Given contracts that account on a ‘macro-promise‘ level (i.e. to build a road), the main question is whether all of the promises within this contract should be bundled together and revenue recognized over time, or if un-bundling is needed and single performance obligations should be recognized upon completion.

Applying the new rules may result in significant changes to the profile of revenue and cost recognition. As a consequence, entities will need to consider implications including changes to key performance indicators, changes to the profile of tax payments as well as changes to compensation and bonus plans.

It is obvious that the search and processing of the relevant information will result in huge efforts and the preparation on the new standard will deeply impact sales support, billing and accounting systems in existing ERP environments, where the relevant business processes and master data are mapped. Therefore, we recommend to define and coordinate the necessary steps and measures promptly.

SAP supports the implementation of these functional challenges with the integrated component Revenue Accounting & Reporting (FI-RA), which receives operative data from the components integrated with it (i.e. sales orders, invoices and order fulfillments, such as goods issues taken from SD module) and – in a rule-based framework – generates the corresponding accruals, deferrals, expenses and revenue postings, which are then transferred to the modules FI and CO-PA and thus keep these components in synch at any time.

We have implemented the basic configuration and prepared the processes around the SAP Add-On Revenue Accounting & Reporting in order to demonstrate an example with you and to pave your way to a straight implementation of the standards in your SAP system.

Resources:

IFRS-16

On January 13, 2016, the International Accounting Standards Board (IASB) published IFRS-16, a new accounting standard for leases.For the lessee, the standard provides a uniform control model in which all operating leases must be brought on-balance sheet.

This applies – more or less – to all lease contracts such as the rental of equipment, servers, production and office space as well as the vehicle fleet.

Thus, lessees can no longer keep a large portion of their financing “off balance sheet” – in the form of operating cost in the income statement – but must recognise a “right of use“ asset and the related lease liability at commencement of the lease with subsequent accounting similar to the finance lease model.

The standard will come into effect in 2019 causing impact on companies that need to review or reevaluate all existing leases and record previously undocumented data for accounting. Technically this implies the adaptation of existing systems and applications, processes and business transactions.

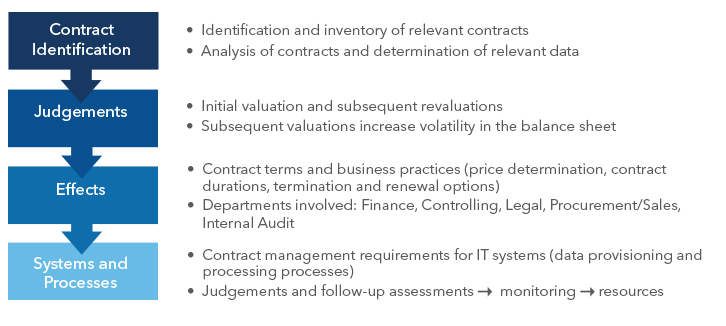

Impact of IFRS 16 on Business Processes

The SAP solution for managing leases is based on an extension of flexible real estate management (RE-FX), which is fully integrated with the General Ledger, Asset Accounting and Controlling.

The solution includes comprehensive contract management and allows:

- set up of different types of contracts and management of business partners

- management of contract terms and tracking of relevant data throughout the contract validity time

- valuation of contracts according to various accounting principles (net present value, depreciation, repayments, etc.)

- support of ledger solution (New General Ledger) and account solution (Classic General Ledger)

- SAP RE-FX-LA is available as an Add-On for SAP ECC and is already part of the standard in SAP S/4 HANA

We have implemented the basic configuration as well as the processes around the SAP RE-FX-LA in order to demonstrate an example with you and to pave the way with you and your auditors for a straight implementation of the standard in your SAP system.

Resources:

Our comprehensive understanding of

SAP® and business insights

enables us to listen, challenge and deliver innovative end-to-end solutions, ensuring the success of your existing and future SAP® investment.

Practical Guide to SAP FI-RA – Revenue Accounting and Reporting Paperback

Accounting standards are changing! Get up to speed and dive into the fundamentals of SAP Revenue Accounting. Review the basic legal principles that determine the reporting of revenues and common technical challenges, as well as the legal basis for ASC 606. Walk step-by-step through the revenue recognition process according to ASC 606. Get best practices on how to prepare your system for an implementation and get a list of activities required to implement the Revenue Accounting and Reporting (FI-RA) business add-on in SAP ERP.